The $3 Trillion Power Grab: Data Centers and the AI Supercycle in 2026

Artificial intelligence isn't just reshaping software.

It's triggering the largest infrastructure buildout in commercial real estate history.

Between now and 2030, the global data center sector requires $3 trillion in capital to keep pace with AI demand. That figure isn't speculation: it's the baseline estimate from JLL's 2026 Global Data Center Outlook, and some analysts believe the real number could push $6.7 trillion when you factor in the full compute power requirements.

This is the AI supercycle. And it's rewriting the rules for developers, lenders, and investors who thought they understood infrastructure.

The AI Supercycle: A $3 Trillion Infrastructure Race

AI workloads are consuming data center capacity at a pace the industry has never seen.

70% of global capacity expansion through 2030 will be driven by AI alone, according to JLL's research. That's not incremental growth: it's a complete recalibration of how hyperscalers, cloud providers, and enterprises allocate computing resources.

The numbers break down like this:

- $1.2 trillion in real estate asset value creation

- $1 to $2 trillion in tenant IT equipment fit-out

- Nearly 100 GW of new capacity between 2026 and 2030

The sector is expanding at a 14% compound annual growth rate, effectively doubling global capacity in the next four years.

For context, that's the equivalent of building every major data center market twice over in less than half a decade.

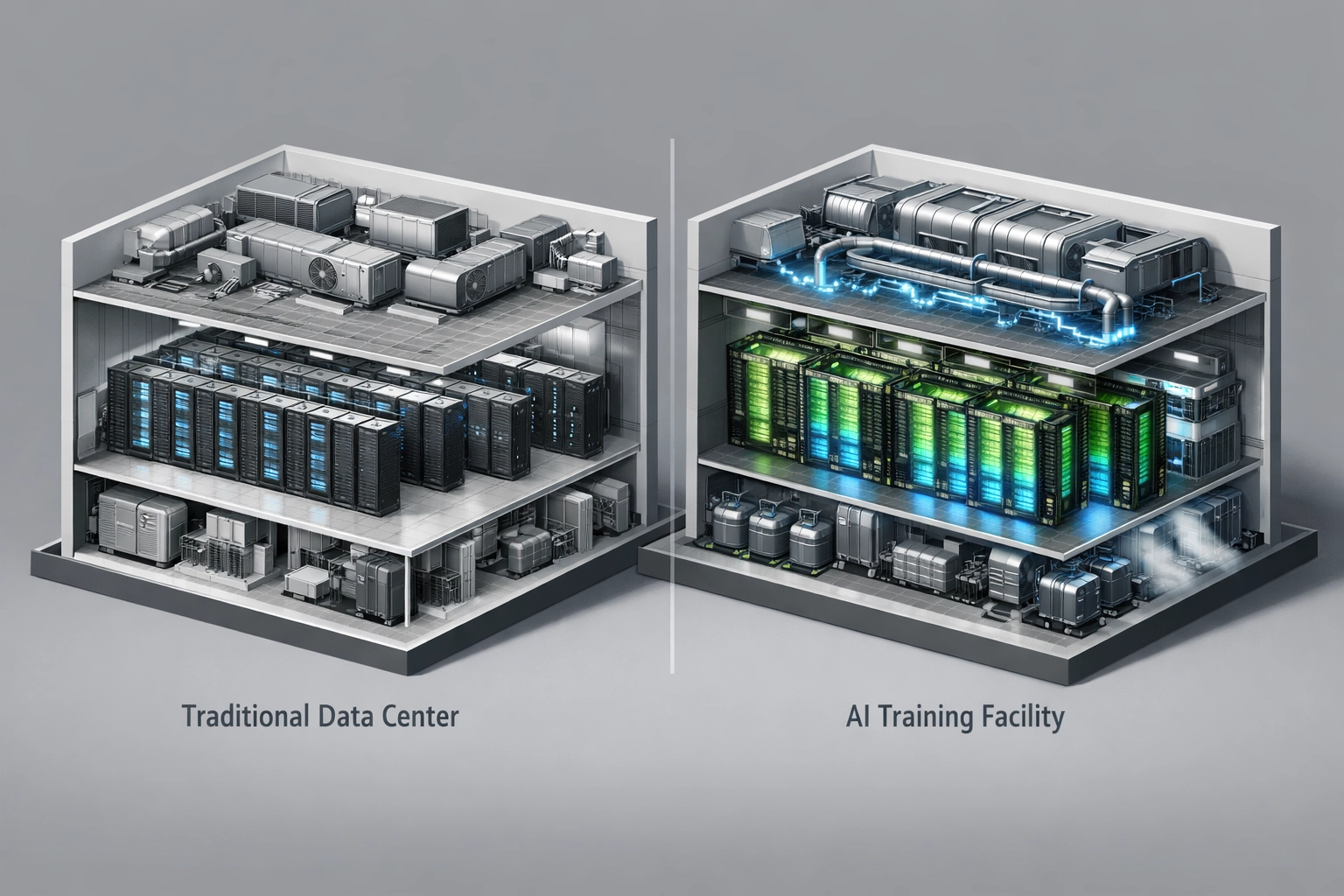

The drivers are straightforward. AI model training requires exponentially more compute power than traditional cloud workloads. JLL flags that next-generation AI training facilities demand 10x the power density of legacy infrastructure.

Translation: The buildings being constructed today are fundamentally different from the colocation facilities built five years ago.

Power Scarcity: The New Land Grab in CRE

Land isn't the bottleneck anymore.

Power is.

CBRE's 2026 Data Center Outlook identifies grid capacity as the single largest development constraint across every major market. Goldman Sachs projects power consumption in data centers will rise 165% from 2023 to 2030, and grid operators in Virginia, Phoenix, and Dallas are already issuing capacity warnings.

Developers are now sourcing sites based on available megawatts, not acreage.

The new calculus:

- Proximity to substations determines site value more than proximity to fiber

- On-site power generation (natural gas, nuclear, renewables) is becoming standard in large-scale builds

- Power Purchase Agreements (PPAs) with utilities are negotiated before land acquisition

Markets with abundant, low-cost power are seeing unprecedented inbound capital.

Ohio, Oklahoma, and parts of the Carolinas are attracting hyperscale projects because their grids can support 50+ MW facilities without major infrastructure upgrades. Compare that to Northern Virginia: the largest data center market in the world: where developers are now facing 3-to-5-year wait times for new power connections in certain submarkets.

This creates a strategic opening for secondary markets.

Investors and lenders who can underwrite power availability as a core asset attribute will capture the next wave of development opportunities.

Doubling Down: Reaching 200 GW by 2030

The scale of the expansion is staggering.

Global data center capacity is projected to hit 200 GW by 2030, up from roughly 100 GW in 2025, per JLL's outlook. That doubling happens in just five years.

Regional growth rates tell the story:

- North America: 17% supply CAGR through 2030 (fastest globally)

- Asia-Pacific: Expanding from 32 GW to 57 GW at a 12% CAGR

- Europe: Stabilizing around 10-11% annual growth, with Frankfurt and Amsterdam leading

Occupancy rates are climbing from 85% in 2023 toward over 95% by late 2026, according to CBRE's research. Pre-leasing activity is through the roof: 77% of the global construction pipeline is already secured by tenants before the facilities break ground.

That level of pre-commitment is almost unheard of in commercial real estate.

It signals two things:

- Hyperscalers are locked in. AWS, Microsoft Azure, Google Cloud, and Oracle aren't waiting for speculative supply. They're securing capacity years in advance.

- Traditional underwriting models don't apply. Lenders evaluating data center debt need to account for tenant creditworthiness and long-term power availability, not just lease-up velocity.

For debt capital providers, this creates a rare combination: strong tenant credit paired with infrastructure-grade cash flows.

If you're structuring construction loans or permanent financing in this sector, you're essentially underwriting utility-like assets with tech company tenants.

Hyperscale vs. Colocation: Who is Winning?

Two business models dominate the data center landscape.

Hyperscalers (AWS, Azure, Google Cloud) are building and leasing massive campus-style facilities, often exceeding 100 MW per site. They're focused on vertical integration: owning or controlling the full stack from power to servers.

Colocation providers (Equinix, Digital Realty, CyrusOne) are leasing turnkey space to enterprises, retail cloud customers, and edge computing deployments. Their model is more diversified, with shorter lease terms and higher tenant turnover.

Right now, hyperscalers are winning the capacity race.

JLL's research shows hyperscalers are driving expansion through dual strategies: direct builds and large-scale lease commitments with third-party developers. They're absorbing supply faster than colocation providers can deliver it.

But colocation isn't dead.

Demand for edge computing: data centers located closer to end users for latency-sensitive applications: is growing at 20%+ annually. Retail colocation facilities in Tier 2 and Tier 3 cities are seeing strong occupancy as enterprises deploy regional AI inference workloads.

The financing implications are distinct:

- Hyperscale deals: Longer-term debt (10-15 years), investment-grade credit, construction-to-perm structures

- Colocation deals: Shorter-term bridge loans (3-5 years), portfolio-level financing, higher leverage tolerance

Lenders who understand these structural differences can tailor capital solutions that match tenant economics and cash flow profiles.

Frequently Asked Questions

Why is AI driving so much data center demand?

AI model training requires 10x the power density and compute resources of traditional cloud workloads. As companies race to deploy generative AI, recommendation engines, and autonomous systems, they're consuming data center capacity at unprecedented rates.

What are the biggest risks in financing data center projects?

Power availability and grid connection timelines are the top risks. Even well-capitalized developers face delays if utilities can't deliver megawatts on schedule. Lenders should underwrite power commitments as carefully as construction budgets.

Are data centers recession-proof?

Not entirely, but they're more resilient than most CRE sectors. Cloud adoption and AI investment tend to be counter-cyclical: enterprises accelerate digital transformation during downturns to cut costs and improve efficiency.

Which markets are seeing the most growth?

Northern Virginia remains the largest, but secondary markets like Phoenix, Dallas, Columbus, and Atlanta are seeing explosive growth due to available power and lower land costs.

Sources

Continue Reading

Have a Deal in Progress?

Let’s structure the right capital solution.