The New Rent Growth Map: Why the Midwest and Northeast are Winning the 2026 Race

The multifamily investment playbook just flipped.

For nearly a decade, institutional capital chased Sun Belt growth. Phoenix, Austin, Dallas, and Orlando promised explosive rent appreciation, population surges, and landlord-friendly fundamentals.

That narrative is over.

According to CoStar's February 2026 rent growth analysis and JLL's Global Real Estate Outlook, the Midwest and Northeast are now the undisputed rent growth leaders: not because of glamorous headlines, but because of one critical factor: supply discipline.

The New Rent Growth Leaders

The numbers are stark.

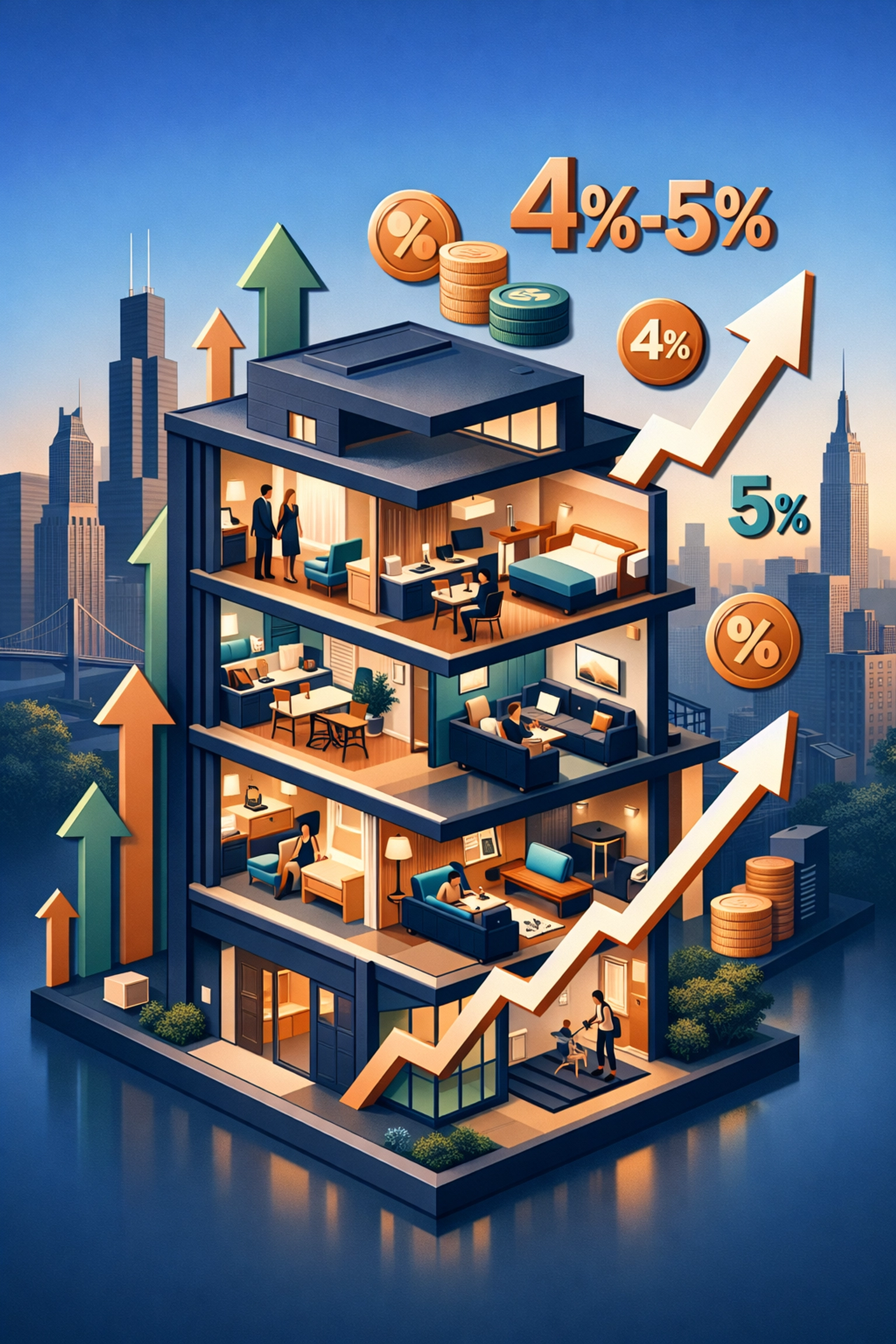

Northeast: 4%–5% projected annual rent growth in 2026.

Midwest: 3%–4.5% projected annual rent growth in 2026.

Sun Belt: 1%–2% as the region crawls out of a year of stagnant or negative rent performance.

West Coast: 2%–3% as supply moderates but remains elevated.

This isn't a temporary blip. It's a structural realignment driven by one undeniable truth: markets that limited development during the construction boom now hold pricing power.

The Northeast benefited from regulatory hurdles, limited developable land, and expensive construction labor. The Midwest maintained discipline thanks to modest population growth and lender caution during the 2021–2023 frenzy.

Meanwhile, the Sun Belt overbuilt. Hard.

The Sun Belt Hangover

Between 2022 and 2025, Sun Belt metros: Austin, Phoenix, Denver, Orlando, and Dallas: delivered unprecedented multifamily supply.

Austin alone added more than 40,000 units in 24 months.

Phoenix saw inventory expansion exceed net absorption by nearly 3-to-1 in certain submarkets.

The result? Landlords chased tenants with aggressive concession packages. Rent growth stalled. Some markets posted outright declines.

For investors holding Sun Belt properties with loans maturing in 2026 or 2027, this is a refinance nightmare. DSCR commercial real estate metrics weakened as revenue flattened while operating expenses: insurance, taxes, labor: climbed aggressively.

CoStar projects that Sun Belt rents will recover to modest 1%–2% growth in 2026, but that recovery is slow, uneven, and heavily reliant on slowing deliveries.

Translation: If you need a refinance in Phoenix or Austin this year, underwriting just got tighter.

Why the Midwest and Northeast Are Built Different

The Midwest and Northeast didn't sit idle during the pandemic boom. They simply didn't overbuild.

Limited new supply in 2025 created a foundation for 2026's rent expansion. Strong metro economies: New York City, Philadelphia, Chicago, and Columbus: provided stable job growth and absorption without the construction bloat.

In the Midwest, affordability remains a magnet. Chicago rents are rising faster than Miami's. Columbus is outperforming Charlotte. Minneapolis is outpacing Nashville.

These aren't sexy markets for Instagram reels. But they are cash flow machines for disciplined investors.

JLL's outlook highlights that Midwest metros offer the best balance of affordability, low construction pipelines, and stable demand. For investors targeting multifamily refinance options with strong debt service coverage, these markets are gold.

The Northeast adds another layer: regulatory barriers to new construction mean supply constraints aren't just a 2026 story: they're baked into the next 5–10 years.

What This Means for Refinancing Strategy

If you own a stabilized multifamily asset in the Midwest or Northeast, your refinance positioning just improved dramatically.

Here's why:

Stronger Rent Growth = Higher NOI Projections.

Lenders underwrite future cash flow, not just trailing 12-month performance. A 4% rent growth trajectory in Philadelphia versus 1% in Dallas translates directly to better LTV and more aggressive proceeds.

Better DSCR Coverage.

Debt service coverage ratio requirements remain firm across the lending universe. But when your revenue is climbing at 4%–5% annually while expenses stabilize, you're hitting lender boxes without requiring heroic rent bumps.

Access to Agency Debt.

Fannie Mae and Freddie Mac remain the gold standard for multifamily financing. Agency lenders favor markets with predictable fundamentals and limited downside risk. Midwest and Northeast assets now fit that profile better than Sun Belt properties battling concession drag.

Bridge Loans Commercial Real Estate Opportunities.

For properties that need time to stabilize before securing permanent financing, bridge loans commercial real estate products are thriving in these regions. Lenders are willing to provide short-term, floating-rate capital to properties in high-growth Midwest and Northeast markets, knowing that the exit to agency or life company debt in 12–24 months is clean.

If you're sitting on a Sun Belt asset, the strategy is different. You may need to extend the maturity, bring fresh equity, or explore mezzanine debt to bridge the gap until rent growth returns.

Regional Performance Deep Dive

Let's break down the commercial real estate trends 2026 by specific metros:

Midwest Winners:

- Chicago: Low pipeline, strong job growth, affordability relative to coastal peers.

- Columbus: Tech hiring, population inflows, negligible new supply.

- Minneapolis: Institutional capital allocating heavily due to supply constraints.

Northeast Winners:

- New York City: Supply limitations, return-to-office momentum boosting demand.

- Philadelphia: Life sciences growth, affordable rent relative to Boston and NYC.

- Boston: Chronic undersupply, educated workforce, limited land availability.

Sun Belt Laggards:

- Austin: Still digesting 2023–2024 oversupply; concessions remain elevated.

- Phoenix: High deliveries continue into Q2 2026; absorption slowing.

- Dallas: Submarket divergence extreme; Class A suffering, Class B stabilizing.

West Coast Mixed Bag:

- Los Angeles: Rent growth returning as deliveries decline.

- Seattle: Tech layoffs moderating but supply still elevated.

- San Diego: Strong fundamentals, but construction pipeline remains a headwind.

The National Rent Picture: A Return to Growth

After a flat 2024–2025 environment, national rent growth is projected to move toward 2.0% on a yearly basis in 2026, according to CoStar.

But that average masks extreme regional divergence.

Markets with tight supply will see 4%–5% growth.

Markets with bloated pipelines will see 1%–2%.

For lenders, this creates a regional underwriting shift. National lending platforms are now applying metro-specific haircuts and growth assumptions rather than blanket multifamily policies.

For borrowers, this means you need to tell a localized story backed by CoStar, JLL, CBRE, or Marcus & Millichap data when pitching refinance requests.

Capital Allocation is Shifting

Institutional investors are reacting.

Pension funds, REITs, and private equity are rotating out of oversupplied Sun Belt markets and into supply-constrained Midwest and Northeast metros.

Why?

Because stabilized cash flow beats speculative appreciation in a refinance-heavy year. When you're managing $200M–$500M in loan maturities, you want predictable revenue, not rent concession risk.

This capital rotation is already visible in Q1 2026 acquisitions. Chicago and Philadelphia multifamily properties are trading at cap rates 25–50 basis points tighter than comparable Austin or Phoenix assets.

Translation: The market is pricing in the rent growth divergence.

Takeaways for Property Owners

If you own multifamily in the Midwest or Northeast:

Refinance now. Rent growth momentum is your friend. Lenders are underwriting aggressively in these markets.

Leverage agency debt. Fannie Mae and Freddie Mac products are wide open for stabilized properties in these regions.

Prepare for appraisal strength. CoStar and JLL data will support higher valuations due to rent growth projections.

If you own multifamily in the Sun Belt:

Expect tighter terms. Lenders are wary of concession risk and oversupply.

Consider bridge financing. Buy yourself 12–24 months for fundamentals to heal before refinancing into permanent debt.

Underwrite conservatively. Don't assume 2022 rent growth returns anytime soon.

Final Word

The 2026 rent growth map isn't about which region has the best weather or the lowest taxes.

It's about supply and demand fundamentals: and right now, the Midwest and Northeast are winning.

For investors navigating multifamily refinance options, this shift creates both opportunity and risk. Position your assets in the right markets, and refinancing is smooth. Miss the regional rotation, and you're fighting headwinds.

Triton Equity Group structures financing for multifamily and commercial assets across all 50 states. If you're evaluating refinance options in today's regionally bifurcated market, we bring lender relationships and market intelligence that ensure you're positioned for success.

Continue Reading

Have a Deal in Progress?

Let’s structure the right capital solution.